Bitcoin doesn’t pay dividends or generate earnings. Traditional valuation metrics don’t apply. For advisors fielding client questions, this creates a problem: how do you assess whether the asset is fairly priced, overvalued, or still has room to grow?

There’s no single answer, but several frameworks have emerged that offer useful reference points. Understanding them won’t settle every debate, but it gives advisors a foundation for informed conversations.

The adoption model

One approach treats Bitcoin as a global savings vehicle and values it based on how many people use it and how much they allocate.

CoinShares’ savings adoption model estimates around 560 million people now own Bitcoin globally, with the US, India, and China among the largest markets. The model assumes owners allocate a small fraction of disposable income- under 1%- and applies a conservative multiplier to translate inflows into market cap growth.

Under these assumptions, the model projects a price floor of roughly $317,000 by 2029. That figure isn’t a target; it’s a baseline derived from measurable adoption trends. If allocation rates rise- say, from under 1% to 1.5%- outcomes shift accordingly.

The appeal of this framework is its grounding in observable data: wallet growth, ETF inflows, survey-based ownership rates. It also highlights the role of emerging markets, where currency instability and limited financial infrastructure have driven adoption faster than in developed economies.

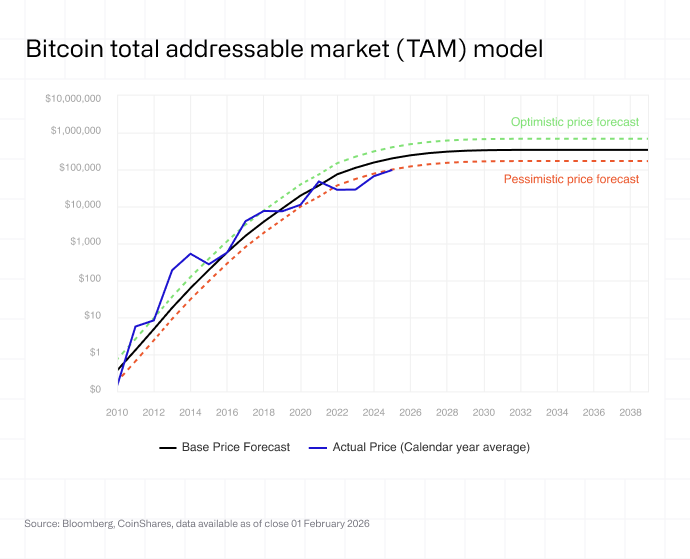

The market share model

A second lens asks: what share of global monetary assets could Bitcoin capture?

This “total addressable market” approach sizes Bitcoin against gold ($22 trillion), global broad money ($119 trillion), central bank reserves ($17 trillion), and corporate treasuries ($6 trillion). Even small inroads into these pools imply significant upside.

At current prices, Bitcoin represents roughly 1% of these combined markets. The question becomes: is that share likely to grow?

Proponents point to structural tailwinds- sovereign debt levels, inflation volatility, the politicisation of dollar reserves- that may push investors toward neutral, non-sovereign alternatives. Sceptics note that Bitcoin remains too volatile and too lightly regulated to serve as a serious reserve asset.

The framework doesn’t resolve this debate, but it clarifies the stakes. A 2% capture of monetary assets implies a price above $200,000 per coin. A 5% capture pushes that figure considerably higher.

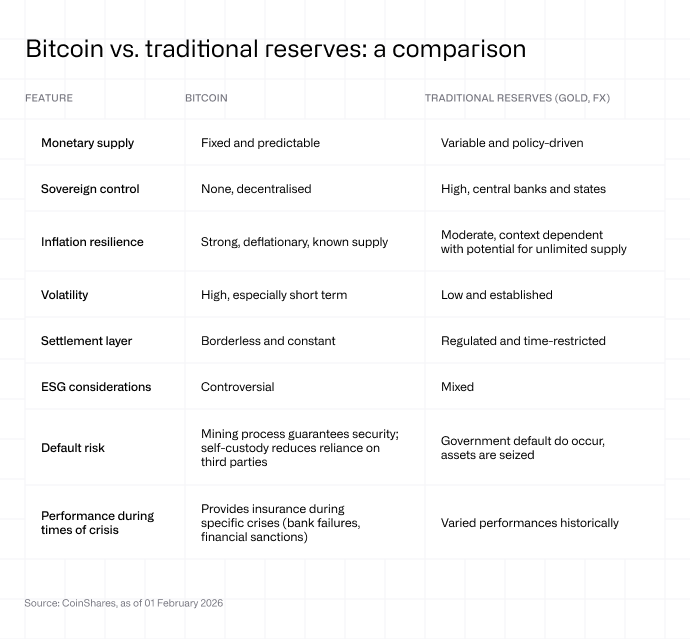

What differentiates Bitcoin

Both models rest on a common premise: Bitcoin has characteristics that distinguish it from traditional assets.

Its supply is fixed at 21 million coins- a ceiling that can’t be adjusted by central banks or governments. Its network has operated with near-perfect uptime since 2009, secured by a decentralised infrastructure resistant to seizure or censorship. It can be transferred globally, instantly, without intermediaries.

These properties don’t guarantee success, but they explain why Bitcoin has attracted a growing share of global savings- and why institutional interest has accelerated since the approval of spot ETFs in the US.

What this means for advisors

Valuing Bitcoin isn’t like valuing equities. There’s no P/E ratio, no discounted cash flow. But that doesn’t mean the exercise is purely speculative.

Adoption-based and market-share models offer structured ways to think about Bitcoin’s potential. They won’t predict next quarter’s price, but they can help advisors contextualise the asset within a broader allocation framework.

Deciding not to allocate is itself a view: a bet that Bitcoin’s share of global monetary assets will stagnate or decline. The bet is audacious as wealth is slowly but surely being transferred to digital native generations, increasingly inclined to embrace digital assets.