Clients are asking about Bitcoin. Guiding them with a clear, intelligible framework has never been more essential.

The conversation has moved on from pure returns potential. What comes up more often is what Bitcoin adds structurally: decorrelation from traditional assets, asymmetric upside, a partial hedge against monetary policy risk. Whether that justifies an allocation depends on the client. But understanding the case has become part of the job.

What diversification actually means here

Diversification works when assets move independently. Bitcoin’s correlation to equities and bonds has historically been low, not zero, but meaningfully different from traditional asset pairs. Its price responds to distinct drivers: fixed supply mechanics, adoption curves, and sentiment cycles that don’t track macro indicators closely.

This matters most when conventional diversifiers disappoint together. When stock-bond correlation rises, portfolios built on that relationship lose their cushion. Bitcoin can provide an offset, though not a guarantee.

Correlation isn’t static, though. Bitcoin has shown periods of higher alignment with risk assets, particularly during broad market stress. The diversification benefit is real, but it fluctuates.

Why volatility isn’t the whole story

Bitcoin remains more volatile than equities. But the magnitude has moderated as the market has matured: deeper liquidity, institutional participation, and a growing cohort of long-term holders have dampened the extreme swings of earlier cycles.

For portfolio construction, volatility is only part of the equation. What matters is how it interacts with everything else. A volatile but decorrelated asset, sized appropriately, can improve risk-adjusted returns even if it moves sharply on its own.

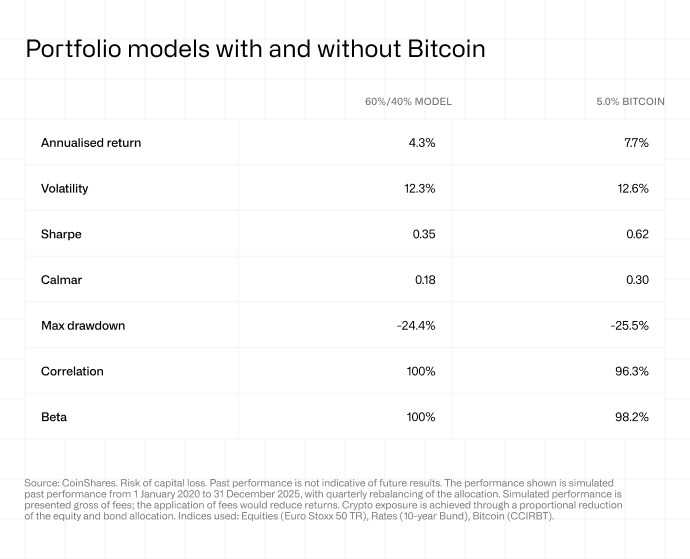

The 5% question

How much exposure makes sense? CoinShares’ modelling points to 5%: with that exposure, historical simulations show improved Sharpe ratios with only a modest uptick in overall portfolio volatility.

The goal isn’t to maximise Bitcoin exposure. It’s to find a level where the diversification benefit outweighs the added complexity, and where drawdowns stay manageable relative to client expectations.

A 5% position can contribute meaningfully if Bitcoin performs. If it doesn’t, the damage is contained.

Rebalancing as discipline

Any allocation to a volatile asset will drift. If Bitcoin rallies, a 5% position can quickly become 8% or more, shifting the portfolio’s risk profile. Regular rebalancing- quarterly, or when thresholds are breached- keeps exposure aligned with intent.

This also enforces a useful behaviour: trimming winners systematically rather than riding momentum. Over multiple cycles, disciplined rebalancing has tended to produce more consistent outcomes than reactive adjustments.

Practical access

For most advisory practices, crypto ETPs offer the cleanest path. They slot into existing custody and reporting infrastructure, removing the operational burden of direct ownership. That simplicity matters when the goal is portfolio integration rather than a broader crypto strategy.

Where this leaves professionals

Bitcoin won’t suit every client or every portfolio. But dismissing it outright is harder to justify than it was, let’s say, three years ago. The asset class has matured, the diversification data is substantive, and client interest isn’t fading.

At 5%, advisors may consider exposure without overcommitting. That may be easier to defend than sitting it out entirely.