Ethereum appears in an increasing number of investment products, market commentary, and client conversations. Yet many advisors remain unclear on what it actually does- and how it differs from Bitcoin.

The short version: Bitcoin is designed to be money. Ethereum is designed to be infrastructure.

What Ethereum does

Ethereum introduced the concept of smart contracts- programs that execute automatically when predefined conditions are met. This programmability turned blockchain from a ledger into a platform, enabling developers to build applications that operate without intermediaries.

The result is a sprawling ecosystem. Decentralised finance (DeFi) applications allow users to lend, borrow, and trade without banks. Stablecoins- digital tokens pegged to fiat currencies- settle hundreds of billions of dollars in transfers each month. Tokenisation platforms are converting traditional assets, from money market funds to real estate, into digital form.

Ethereum dominates these use cases. It accounts for over half the total value of tokenised real-world assets and the majority of stablecoin supply. Major institutions- BlackRock, Franklin Templeton, Standard Chartered- are building on its rails.

How it differs from Bitcoin

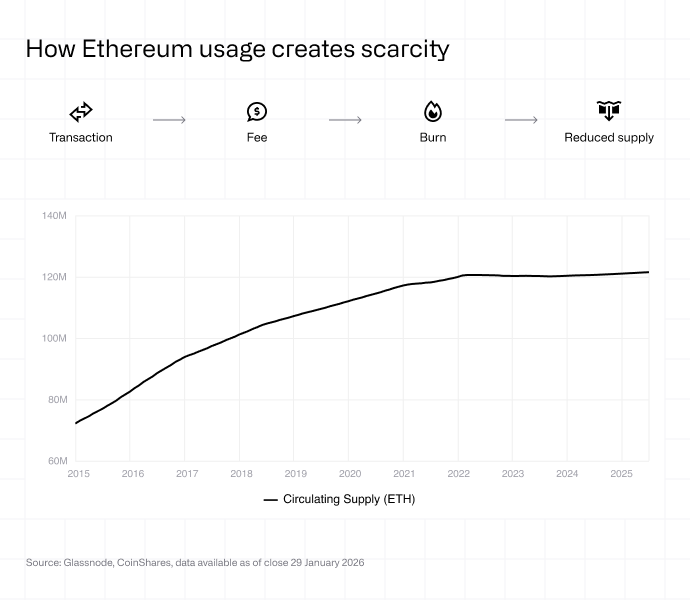

Bitcoin’s monetary policy is fixed: 21 million coins, ever. Ethereum has no hard cap, but it burns a portion of transaction fees, making its supply dynamic and tied to network usage. When activity rises, more ether is destroyed than created, introducing a deflationary pressure.

The networks also secure themselves differently. Bitcoin relies on proof of work, where miners compete to solve computational puzzles. Ethereum shifted to proof of stake in 2022, requiring validators to lock up ether as collateral. The change cut energy consumption by over 99% and allowed holders to earn yield by staking their tokens.

These differences shape how the assets behave in portfolios. Bitcoin tends to trade as a macro hedge and store of value. Ethereum’s price is more closely tied to on-chain activity and the growth of its application layer.

Where finance is heading

What’s notable isn’t just that institutions are experimenting with Ethereum- it’s where the experiments are pointing.

Tokenised funds are the first step. But the longer-term trajectory is toward on-chain issuance, where securities are natively created on blockchain rails rather than converted after the fact. Settlement cycles that currently take days could collapse to minutes. Custody, clearing, and reconciliation- functions that employ thousands and cost billions- could be automated through smart contracts.

This isn’t speculative. Bank of America has called tokenisation “mutual fund 3.0.” The EU’s MiCA regulation and Pilot Regime are creating legal frameworks for on-chain securities. Switzerland and Singapore are already operating under clearer rules.

Ethereum’s role in this shift is not guaranteed, but it’s head start is real: the largest developer community, the deepest liquidity, and the widest institutional footprint. Competing chains exist, but most major financial pilots to date have chosen Ethereum or networks built on top of it.

Risks to consider

Ethereum itself has proven to be resilient but its ecosystem is not without vulnerabilities. Smart contract exploits have led to significant losses: hackers regularly target bugs in application code or the data feeds that connect blockchains to external information.

And then there’s competition. Solana, Hyperliquid, Avalanche, and newer entrants are vying for developer attention. Ethereum’s lead is substantial, but not guaranteed.

Where this leaves advisors

Ethereum isn’t a second Bitcoin. It’s a different bet: on programmable finance, on tokenisation, on infrastructure that may underpin the next generation of financial products.

For advisors, understanding the distinction matters. Holding both assets is complementary, not redundant.